After months of anticipation, in July 2023 EFRAG finally published the final European Sustainability Reporting Standards (ESRS) Delegated Act in a single 245 page document.

This is the moment companies subject to the Corporate Sustainability Reporting Directive (CSRD) have been waiting for, as they prepare to issue their first ESRS-compliant non-financial reports, the biggest companies already for 2024.

While the draft standards published in November 2022 were considered a near-final version, companies were hesitant to move forward before seeing the final version of the document. Now that the final standards are available, as well as some guidance documents, companies can feel more confident about kicking off their materiality and data collection processes to begin preparing for reporting.

Below is an overview of some of the key points to know about the final version of the ESRS, including some changes made compared to the draft standards.

Table of contents:

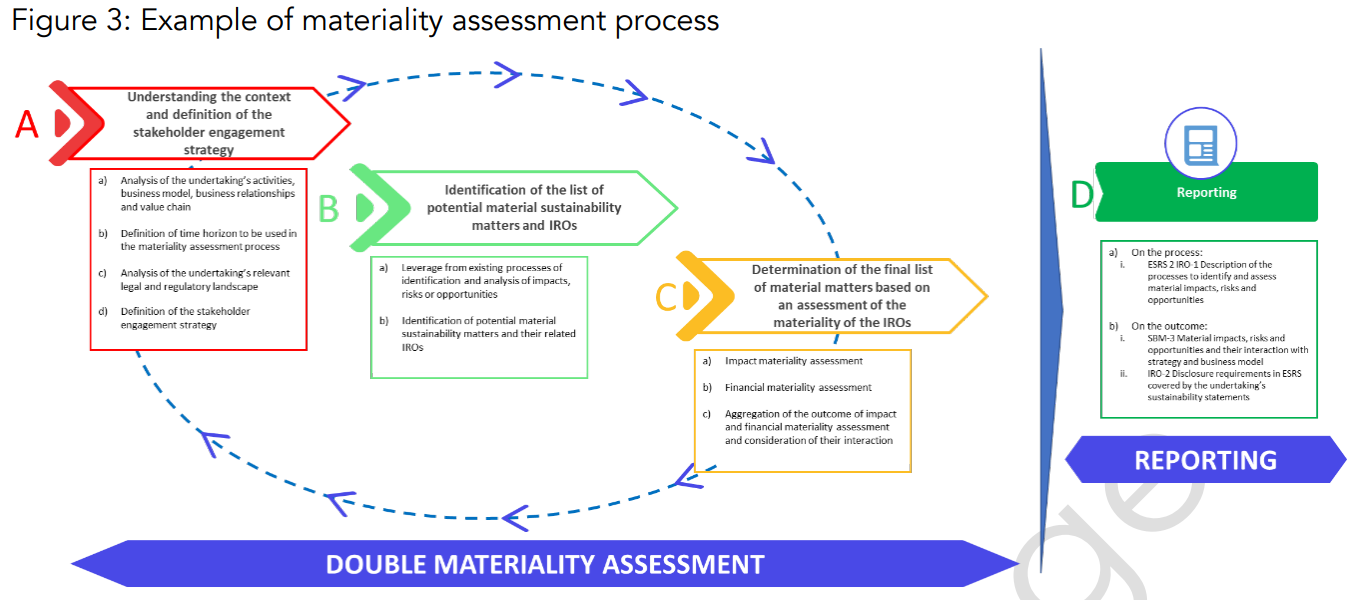

Double materiality remains the foundation of sustainability reporting according to ESRS. Shortly after publication of the final ESRS, EFRAG released a double materiality guidance draft document (which is still to be revised and finalized by EFRAG). The document details how companies should determine which of the topics, subtopics, and sub-subtopics found in Appendix A of ESRS 1 (together “sustainability matters”) are material to their business from the perspective of positive/negative impacts or opportunities/risk.

There is no formally prescribed methodology for a double materiality assessment, but in general it must include:

- Internal and external stakeholder engagement;

- Assessment of the materiality of impacts based on their severity, which is a combination of:

scale, scope, remediability and likelihood in the case of potential negative impacts;

scale and scope for actual positive impacts;

scale, scope and likelihood for potential positive impacts;

- Assessment of the materiality of risks and opportunities, which is based on a combination of the likelihood of occurrence and the potential magnitude of the financial effects.

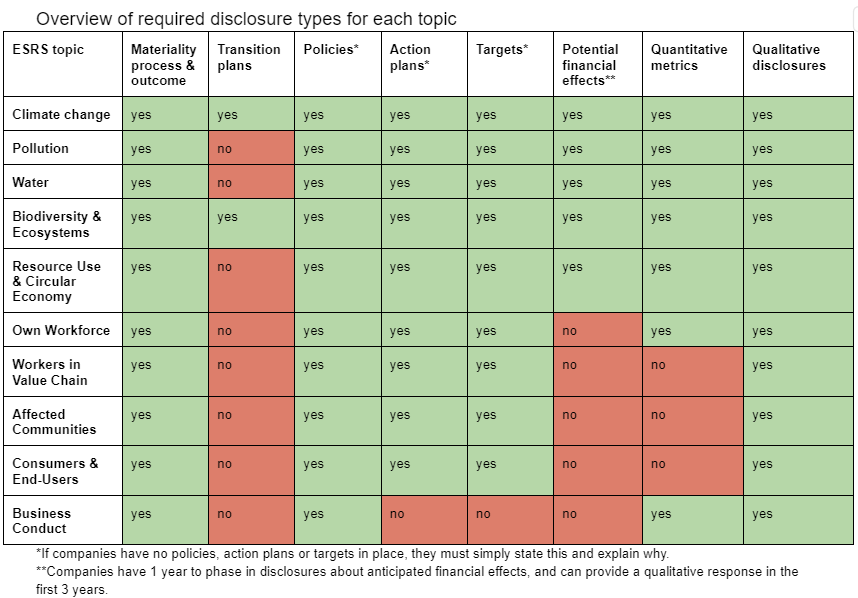

In total, the 12 chapters of the ESRS contain over 80 disclosures, and over 1000 both quantitative and qualitative data points related to those disclosures. It is no longer mandatory for all companies to report the disclosures in ESRS E1 Climate Change and selected disclosures from ESRS S1, Own Workforce – these disclosures are now only required if found to be material. Only disclosures from ESRS 1 General Disclosures are mandatory for all companies regardless of the outcome of the materiality assessment. As before, all disclosures relating to material topics, subtopics and sub-subtopics are mandatory to report, with the following caveats:

- Any disclosure stating that a company “may” rather than “shall” report data, is not mandatory even if the disclosure is material. The number of optional disclosures increased in the final version of the standards.

- If companies do not have policies, action plans or targets in place to manage material topics, they may simply state this and may optionally share when they plan to do so.

- Some disclosures can be phased in over 1-2 years.

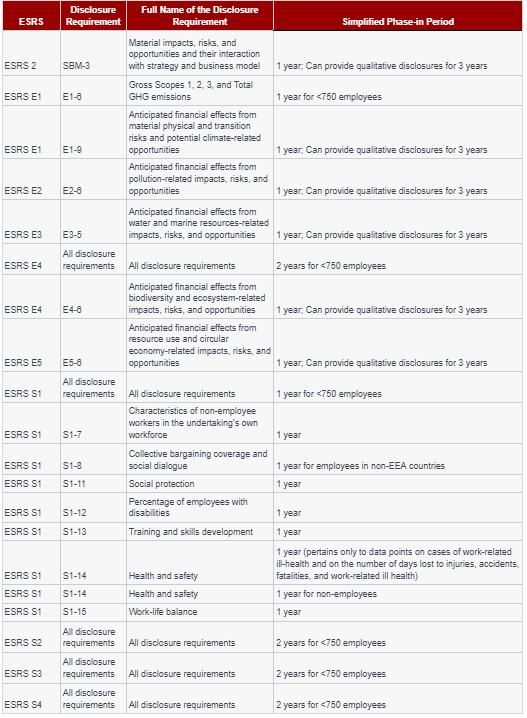

In the final version of the ESRS, more time was built in to help companies, particularly those with fewer than 750 employees prepare the necessary data. A full list of disclosures that can be phased in can be found in Appendix C of ESRS 1 (page 29 of the document), and we have recreated a simplified version below:

EFRAG newly introduced “minimum disclosure requirements” into ESRS 1 General Disclosures to detail what should be reported regarding policies, action plans, metrics and targets for each topic where it is required. Further details about how to report policies, targets and action plans can be found in topical chapters; e.g. the Climate Change chapter contains further details about how companies should report on climate-related risks, as well as what exactly should be included in the climate transition plan.

The ESRS provides companies with a 3-year phase-in period to include information from their upstream and downstream value chain.

“For the first 3 years of the undertaking’s sustainability reporting under the ESRS, in the event that not all the necessary information regarding its upstream and downstream value chain is available, the undertaking shall explain the efforts made to obtain the necessary information about its upstream and downstream value chain, the reasons why not all of the necessary information could be obtained, and its plans to obtain the necessary information in the future.” (ESRS 1, paragraph 10.2, p. 20)

However, in their fourth year of reporting, companies will be required to include data from their value chain when reporting information about policies, action plans, targets and metrics. EFRAG has published a value chain guidance document to help companies understand how to report on their value chain.

ESRS 2 Appendix B contains a list of datapoints required by EU law. If these are found to be not material, it is required that companies explicitly state this. Companies must provide a table in their sustainability report indicating where each datapoint can be found in the report, or if not material, then it must state this.

EFRAG provides a required structure for the report, which they call the “sustainability statement,” to help facilitate comparability of reports. The structure is as follows:

- General information

- Environmental information

- Social information

- Governance information

In conclusion, the final ESRS provides some breathing room to companies via phase-in periods and a reduced number of mandatory disclosures. However, the amount of data companies will have to report in the first year is still huge and will require significant effort and collaboration. It is recommended that companies begin now to pull together the required data and internal teams to oversee the materiality, data collection and reporting processes.

Further reading

(Image by fabrikasimf on Freepik)